There's no doubt that college is expensive. Just ask any parent currently helping their son or daughter find a college or file the FAFSA.

How to save and pay for college is a central question for most families - particularly millennial parents and older members of Gen Z. While politicians debate college affordability at the national level, families often feel like they are on their own to navigate the process of planning and paying for college for their family.

Let's explore some basic concepts of financial literacy that may help manage future decisions about how to plan and pay for the dream college for your children:

- Managing your budget

- Making a plan

- Using compounding to your advantage

- Identifying wants, needs, and value

Managing Your Budget

Parents who recently started a family may also be dealing with their student loans. Some may have just paid off their loans. Others are in the process. Anyone with a child has the added concern of how to also start socking away some money for future college costs.

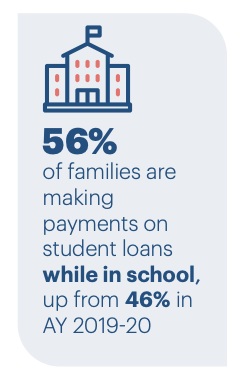

According to Salle Mae's report, "How America Pays for College 2021" many have practiced a very sound financial literacy teaching to reduce debt: 56% of families made payments on loans while in school. This strategy significantly reduces the total cost of a loan and creates additional cash flow.

Families with young children often struggle to balance between allocating income for current needs, paying off their debts, and saving for their retirement and their children's college. Many are very wary of how student debt affected them and seem to have spurred the current trend toward increased college savings. As the national debate over student loans and college affordability continues, families are taking control of their savings plans to make a smarter and more affordable investment in higher education.

Making a Plan

Planning to save and pay for college can begin at any time. The plan does not have to be a twenty-page strategic plan with graphs and projections. A simple, high-level understanding of the cost of college, how - and how much - to save and the options to pay will be valuable. The Sallie Mae report also noted that 58% of families have a plan to pay for all years of college, up 14% in the past two years.

Part of the plan should include understanding the cost of the goods or services to be purchased. It's now easier than ever before to make and compare estimates of college costs, student loan repayment, and savings. Families can get a good look at the big picture before diving into the details of how to pay the bill from a particular school. No matter the age of a student, considering questions like financial aid eligibility and how the aid will reduce the sticker price of a college will help you plan to save and pay for college. The sticker price is the advertised price you can find on the school's website. The amount you pay, i.e., the net price, is the sticker price less financial aid. This amount will be different for each college.

A school with a big sticker price and generous financial aid may be more affordable than a lower-priced school that offers less financial aid. Parents can use free financial calculators like this one to get some idea of the net price they may be asked to pay. Of course, everyone's income and financial situation will change, perhaps considerably, by the time today's five-year-olds apply to college. However, some planning now will help parents better understand how much their projected savings will help them in the future.

With this information, parents can then determine how best to save and plan for college. This free College Savings Estimator will help you estimate an appropriate amount to save.

Using Compounding to Your Advantage

Long-term savers understand a very important financial literacy concept. Overtime money grows with the power of compound interest and asset appreciation. The longer the savings horizon, the greater the potential to increase savings.

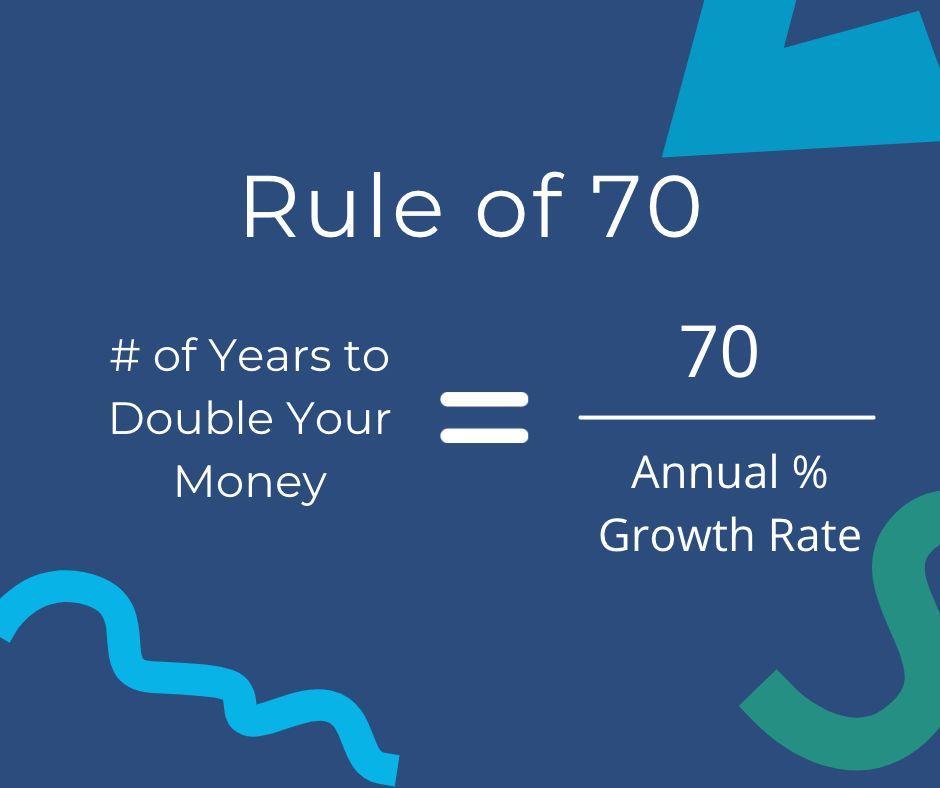

One very simple way to easily estimate savings is to use The Rule of 70. It is a financial concept that predicts how long it will take to double your savings:

For example: if you earn 7% interest annually, your money will double in 10 years. On the other hand, if you know that you have 20 years to double your savings, you need to earn 3.5% interest per year.

While financial calculators help with the details, the impetus behind saving begins with the motivation to start early, rather than later, to make college more affordable.

Identify Wants, Needs & Value

Know thyself!

If financial literacy can teach us one thing, it is that everyone makes choices based on their wants and needs. This is true for small everyday purchases as well as for big purchases such as a college education.

Deriving value from a college education is different from deriving value from other purchases. A good portion of college value depends on individual factors managed on the personal level. When weighing the many "soft" variables, such as majors, school reputation, and internships, and comparing them to quantitative measures such as sticker price, costs, student loan debt, and job placement rates, patterns of affordability (and value) will emerge. Some colleges will be too expensive while others may be a bargain relative to the needs of the student.

For families with younger children, considering value is not immediately relevant. The primary objective is to determine how to be best positioned to save for college among many competing priorities. Knowing the cost of college in the future and making a high-level plan, including savings, to pay for college is an important first step.